Many people believe that SPAXX is fully state tax exempt in the US.

Not so fast!

There’s a quick, but important, tax nuance that’s easy to miss if you hold Fidelity cash / mutual funds like SPAXX, particularly if you live in three specific states.

A lot of people hear “government money market” and assume the dividends are state tax-exempt. The reality is more subtle:

The reality about SPAXX State Tax Exemptions

Here’s what is true: many states will let you exclude the portion of a fund’s ordinary dividends that came from U.S. government securities (like Treasuries, certain government-backed holdings, etc.). Fidelity publishes a yearly worksheet showing the percentage of each fund’s dividends attributable to U.S. government securities and gives an example of how to calculate the potentially state-exempt amount.

Example:

If you earned $1,000 in ordinary dividends from a fund and the worksheet says 26.41% eligible U.S. government securities income, then $264.10 may be state tax-exempt.

So far so good, right?

The big mistake (where people get tripped up)

Some states don’t just look at the “percentage of eligible government income.” They require a minimum threshold of U.S. government securities exposure before they’ll allow any state tax exemption for the distribution.

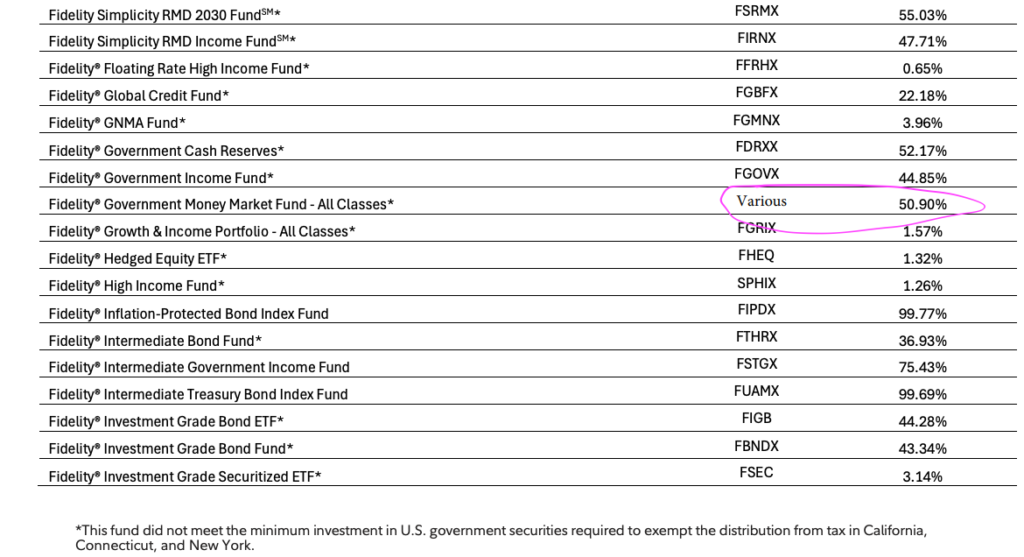

So, what do we see when we look at this Fidelity disclosure?

We can see that just over half of these money market funds are in the relevant government adjustments.

What does this mean practically?

Fidelity calls this out directly:

- California, Connecticut, and New York only exempt that dividend income if the fund meets a minimum investment thresholdin U.S. government securities.

- In Fidelity’s worksheet, funds marked with an asterisk (*) did not meet that minimum threshold for CA/CT/NY — meaning those states may treat the dividends as fully taxable at the state level, even if some portion came from U.S. government securities.

This is the part many investors miss:

A fund can have “some” government securities income, but still fail the state threshold and give you zero exemption in CA/CT/NY.

How to use Fidelity’s worksheet correctly

- Find your ordinary dividends for the fund on your 1099-DIV (Fidelity shows you where to find it depending on account type).

- Multiply that dividend amount by the fund’s “% eligible income from U.S. government securities.”

- Then apply the state-specific rule:

- In many states, that calculated portion may be exempt.

- In CA/CT/NY, if the fund has an asterisk, you may not get the exemption at all.

Bottom line

If you’re in California, Connecticut, or New York, don’t assume “government fund” automatically equals “state tax-free.” The fund’s percentage does matter, but the threshold rule can matter even more — and it can turn a “partially exempt” expectation into “fully taxable.”

As always, this is general education, not tax advice — state rules are finicky and change. If it’s meaningful dollars, it’s worth confirming with your CPA or tax software prompts. Just thought I would help you guys out!