Your emergency fund shouldn’t just be a static pile of cash.

You certainly shouldn’t leave it in a checking or savings account with paltry interest. God forbid!

The savvy are content to leave it in a money market fund or a high-yield savings account, which I believe is perfectly reasonable.

But if you don’t mind about 5 minutes of work each month, and you live in a high tax state, You can achieve a stronger return with a zero-coupon Treasury Bill ladder.

The goal here isn’t just a slightly higher yield; it’s about maximizing tax efficiency. By using zero-coupon 1-month Treasuries instead of a money market fund, I can capture a higher base rate and avoid state and local taxes entirely.

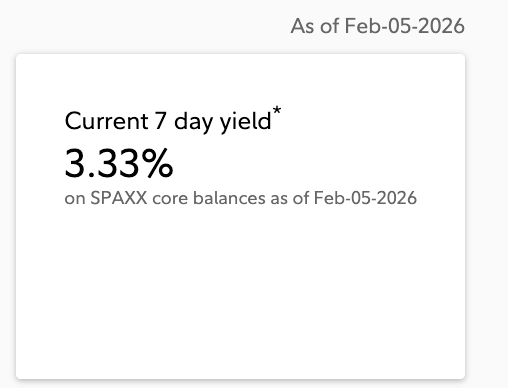

The Real Data: SPAXX vs. 1 Month T-Bills

As of early February 2026, the Federal Reserve has held rates steady, but we are seeing a widening gap between what money market funds pay out and what you can get by going directly to the Treasury.

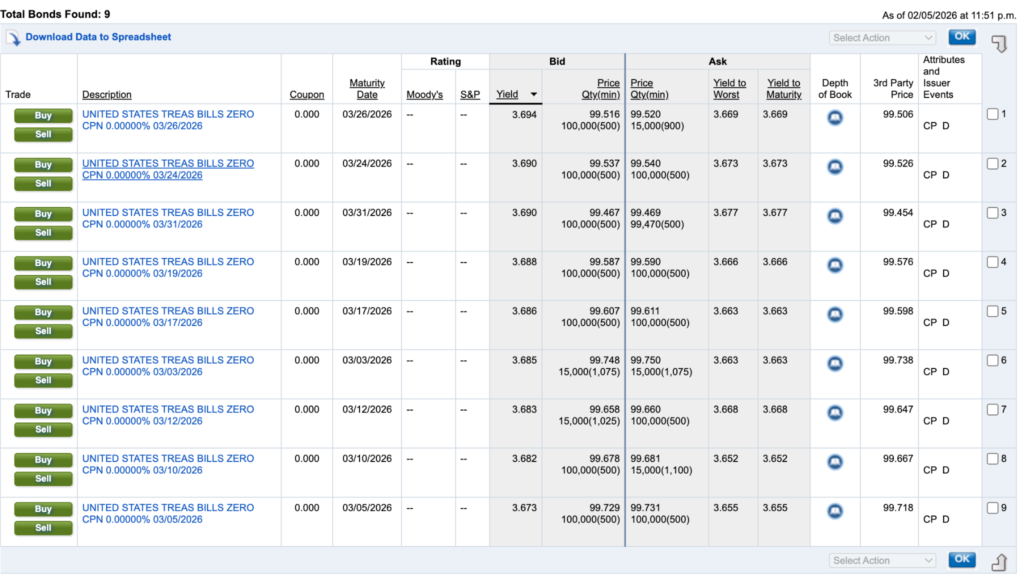

For example, let’s look at the gap in March for estimated SPAXX yield and the one-month zero-coupon T-bill yield.

Spaxx is hovering around 3.33% right now with Fidelity.

And you can see the higher yields on the March 0 coupon Treasury bills below.

That leaves us with about a 0.36% difference.

| Month (2026) | SPAXX Yield (Est.) | 1-Month T-Bill Yield | Spread |

| March | 3.33% | 3.69%* | +0.36% |

*Projections based on current Fed dot plots and 1-month constant maturity yields.

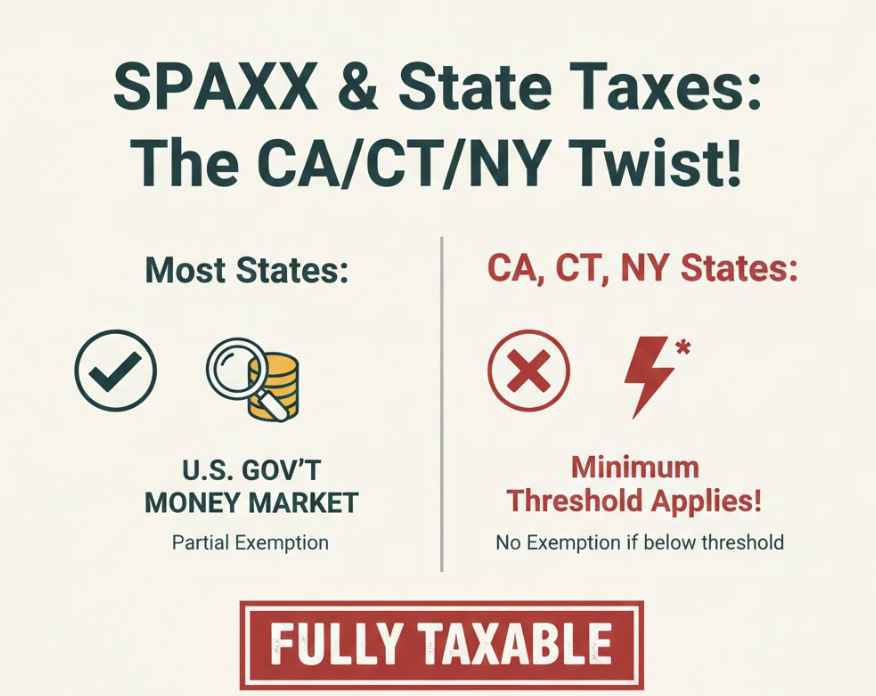

The “Hidden” Savings: The State Tax Advantage

The headline yield is only half the story. The real reason I favor this strategy is the state tax exemption. If you live in a state with an income tax, a money market fund like SPAXX is a drag on your performance. For example, in California you might sit around 7%. That can eat into your returns year over year!

| Instrument | Yield | State Tax Status |

| SPAXX (Money Market) | 3.33% | Fully Taxable |

| 1-Month T-Bill | 3.69% | 100% Exempt |

The Comparison: A $25,000 Emergency Fund

To see the actual impact, let’s look at how this plays out over a year for a $25,000 emergency fund. We’ll use an effective 7% for State Income Tax and 25% for Federal.

Scenario A: The Money Market (SPAXX)

- Annual Interest: $832.50

- Total Tax Hit (32%): $266.40

- Take-Home Cash: $566.10

Scenario B: The 1-Month Treasury Ladder

- Annual Interest: $922.50

- Federal Tax (25%): $230.63

- State Tax (0%): $0.00

- Take-Home Cash: $691.88

The Result: By moving to a T-Bill ladder, you’re putting an extra $125.78 in your pocket annually. It’s a “risk-free” raise that takes about 10 minutes to set up.

The 6-Month “Always-On” Ladder Setup

If you have a six-month emergency fund (let’s say $25,000 total), you want to divide that into six equal “rungs” of approximately $4,166. These zero-coupon bills are bought at a discount and then appreciate over the duration of their lifetime back to full par value, so there’s no interest exactly per se, and you can sell at any time along the appreciation curve back to full par. Here is how I build the initial momentum:

- Month 1 (The Launch): I buy six 1-month (4-week) Treasury bills. This gets the full $25,000 working immediately at that higher 3.69% rate.

- Month 2 (The Stagger): As those bills mature, I take the first $4,166 and roll it into a new 1-month bill. I take the rest and do the same, ensuring I select the “Auto-Roll” feature.

- The Result: Because Treasury auctions happen weekly, you can time your purchases so that exactly one-sixth of your fund expires every 30 days.

Why I prefer this structure

By always having one month’s worth of expenses ($4,166) expiring, I never have to worry about a “lock-up.”

- If life is normal: The bill matures, the “Auto-Roll” kicks in, and the money is immediately reinvested into a new 1-month bill at the current market rate.

- If an emergency hits: I simply go into my brokerage account and “cancel” the auto-roll for the upcoming maturity. Within days, that month’s cash is sitting in my sweep account, ready to be spent.

The “Auto-Roll” Advantage

Most major brokerages (like Fidelity or Schwab) make this incredibly easy. Once you set the initial ladder, you don’t have to log in every month to buy new notes. The system handles the heavy lifting, ensuring your $25,000 is always capturing that 3.69% yield and staying 100% exempt from that 7% state tax.

It takes a little bit of front-end work to time the initial purchases, but once the cycle is moving, you’ve built a self-sustaining, tax-advantaged machine that outperforms a standard money market fund every single day of the week.

A Final Note

We focused on the emergency fund here, but you can imagine how valuable this could be with much larger amounts of money. For example, when you’re starting to transition into cash for a home purchase but are still a few months out from it, or when you receive a large inheritance or bonus but aren’t sure where to deploy yet. You can squeeze out a little bit of extra performance, and that can add up in the long run!